Work Permit Application Types and Their Tax Implications

2026/05/13

- I-GLOCAL.CO.,LTD Hanoi Office

- Vu Thi Huong Giang

Executive Summary

Many Japanese-invested enterprises in Vietnam have historically obtained work permits for expatriate employees under the “intra-company transfer” type while continuing to pay them salary and benefits from the Vietnamese entity. However, recent regulatory developments in 2025 have made it essential to align the work permit type with the actual arrangement — specifically, whether or not wages are paid locally.

Key Points

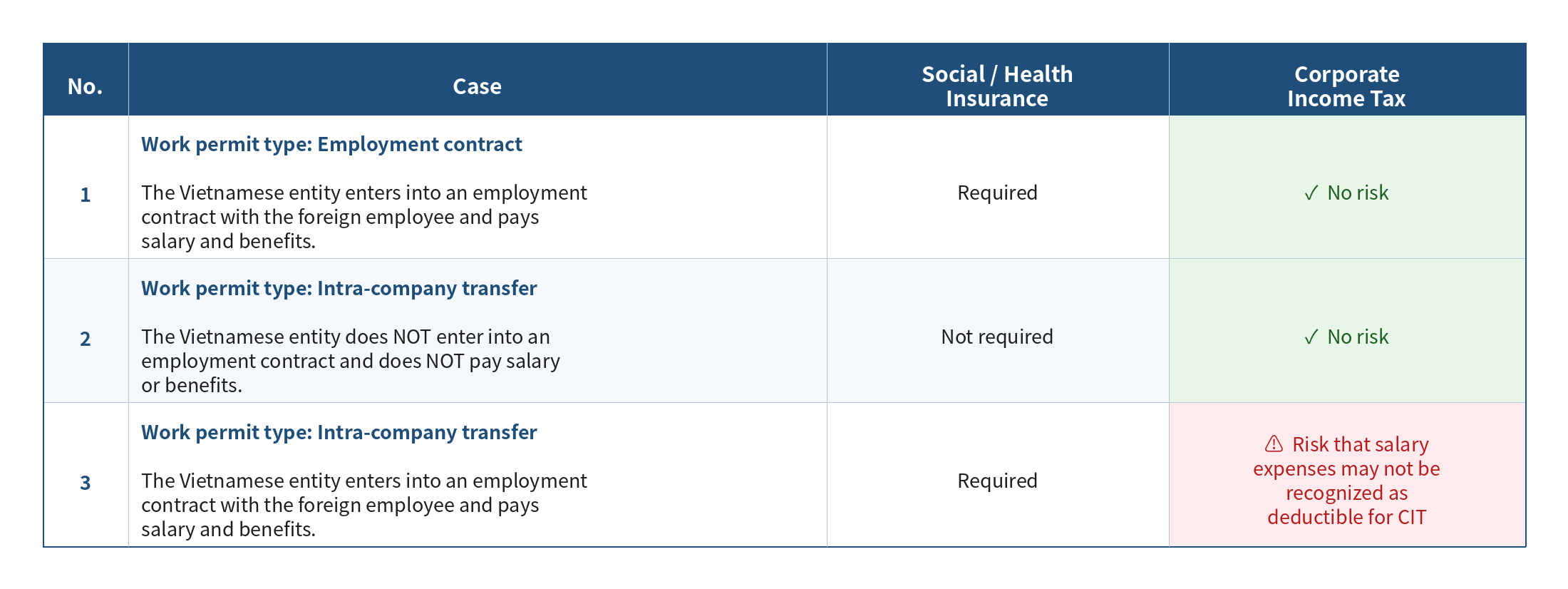

・[Two Types Clarified] Under Official Letter No. 10861/BNV-CVL (November 2025): (1) Foreign employees receiving wages from a Vietnamese entity → “Employment contract” type: must sign an employment contract and enroll in Vietnamese social insurance. (2) Foreign employees dispatched from the parent company without receiving local wages → “Intra-company transfer” type: no employment contract or social insurance enrollment required.

・[CIT Risk] Decree No. 320/2025/ND-CP added the dispatch/appointment letter as a valid tax document for intra-company transfers, but this is not consistent with the MHA’s position. Where a work permit is obtained under the intra-company transfer type but the Vietnamese entity pays wages, those salary costs risk being disallowed as CIT deductions (see Case 3 in the table below).

・[Housing & School Fees] Deductible for CIT only where the Vietnamese entity has signed an employment contract with the foreign employee explicitly providing for these benefits, supported by appropriate documentation.

・[Recommended Action] If paying wages: apply for work permit under the “employment contract” type and sign an employment contract (mandatory social insurance enrollment applies). If not paying wages: maintain the intra-company transfer type without an employment contract. The most critical point is to avoid the mismatch between the work permit type and actual practice (Case 3).

Introduction

Many Japanese-invested enterprises in Vietnam receive expatriate employees dispatched from their parent companies abroad under an intra-company transfer arrangement. In most cases, the Vietnamese entity provides the foreign employee with various allowances and benefits, including housing, living expenses, transportation, meal allowances, and in some cases a portion of their salary. Given that labor authorities have been tightening their oversight of these arrangements in recent years, whether such payments are permissible under labor law and deductible as expenses for corporate income tax (CIT) purposes has become an increasingly important issue. This report explains the types of work permit applications and their respective tax treatment.

1. Regulatory Framework on Work Arrangement Types

In Official Letter No. 10861/BNV-CVL dated November 19, 2025, the Ministry of Home Affairs (MHA) clarified its interpretation of the nature of labor relations and employment contracts under the Labor Code, and distinguished between the different types of work permits applicable when foreign employees work in Vietnam. A summary is as follows:

Foreign employees working at and receiving wages from Vietnamese enterprises or organizations:

Prior to the expected start date of employment, the employer must apply for a work permit for the foreign employee, enter into an employment contract in accordance with labor legislation, and register the employee for social insurance in Vietnam in accordance with social insurance legislation.

Foreign employees dispatched under an intra-company transfer arrangement:

This refers to a temporary internal transfer within a foreign enterprise that has established a commercial presence (*) in Vietnam, covering the 11 service sectors under Vietnam’s WTO service schedule commitments. The foreign employee must also have been continuously employed by the foreign enterprise for at least 12 consecutive months prior to the transfer.

(*) Commercial presence includes foreign-invested economic organizations; representative offices and branches of foreign traders in Vietnam; and operating offices of foreign investors under business cooperation contracts (as defined under Article 13, Clause 13(b) of Decree No. 219).

Based on the above, under the Labor Code No. 45/2019/QH14 and related guidance documents on foreign employees working in Vietnam, two distinct cases can be identified: (1) foreign employees who receive wages in Vietnam, and (2) foreign employees dispatched under an intra-company transfer arrangement.

From this analysis, foreign employees who receive wages in Vietnam are considered to have an employment relationship with the Vietnamese enterprise. They are therefore required to enter into an employment contract with the Vietnamese entity in accordance with labor legislation, and the applicable work permit type is “performance of employment contract.” Mandatory enrollment in Vietnamese social insurance also applies in this case.

In contrast, an intra-company transfer is a personnel arrangement whereby an employee is temporarily dispatched to Vietnam from the parent company for a fixed period, and does not presuppose payment of wages by the Vietnamese entity.

2. CIT Provisions on Wages and Remuneration

Under the current CIT regulations (Decree No. 320/2025/ND-CP, effective December 15, 2025), salary, wages, and wage-like allowances paid to employees are deductible for CIT purposes only if all of the following conditions are met:

- Actually incurred and related to the enterprise’s production and business activities;

- Supported by valid invoices and documents in accordance with applicable regulations;

- Supported by non-cash payment documentation for individual payments of VND 5,000,000 or more;

- The entitlement conditions and benefit levels are clearly specified in one of the following documents:

– The employment contract, or a document issued by the foreign enterprise dispatching the individual to work in Vietnam (*) (applicable to cases of intra-group transfers or intra-company transfers between a parent company and its subsidiaries);

– The collective labor agreement; or

– The enterprise’s financial regulations or bonus policy.

Housing allowances and school fees for the children of foreign employees (for education in Vietnam from preschool through upper secondary school) are deductible for CIT purposes, provided that the Vietnamese entity has entered into an employment contract with the foreign employee, the relevant benefits are explicitly specified in the contract, and appropriate supporting documents are maintained.

While Decree No. 320/2025/ND-CP added the dispatch letter (appointment letter) for foreign employees in intra-company transfer cases as a valid document for tax purposes, this position is not consistent with the interpretation and guidance issued by the Ministry of Home Affairs.

Accordingly, even where a Vietnamese entity pays wages to a foreign employee on an intra-company transfer and clearly specifies the entitlement conditions and benefit levels in the appointment letter, there remains a risk that such payments may not be recognized as deductible expenses for CIT purposes, if they are determined to be non-compliant with the relevant labor legislation.

3. Conclusions and Recommendations

Based on the current regulatory framework and the prevailing approach of the relevant authorities, the risks associated with salary, remuneration, and benefit expenses for intra-company transfer foreign employees can be summarized as follows:

Based on the above analysis, in order to mitigate risks from both a labor and tax perspective, enterprises should review and select the appropriate work arrangement type for foreign employees when applying for a work permit.

Accordingly, where an enterprise continues to apply for a work permit under the intra-company transfer type as before, the appropriate approach going forward is for the Vietnamese entity not to enter into an employment contract with the foreign employee and not to pay wages to that individual.

Conversely, where an enterprise pays wages to a foreign employee, it must apply for a work permit under the “performance of employment contract” type and enter into a corresponding employment contract. In this case, it should be noted that the foreign employee will be subject to mandatory social insurance and health insurance enrollment in Vietnam.

Conclusion

This report has explained the types of work permit applications and their respective tax treatment. As the current regulatory framework differs from prior practice in many respects, enterprises are advised to review the relevant legislation and determine the appropriate course of action from both a labor and tax perspective.

Reference

・Decree No. 219/2025/ND-CP (dated August 7, 2025)

・Official Letter No. 10861/BNV-CVL (dated November 19, 2025)

・Decree No. 320/2025/ND-CP (dated December 15, 2025)

Related Reports

・Amendments to Decree 219/2025/ND-CP Concerning the Procedures for Issuing Work Permits to Foreign Workers

・Points to Note About Full Remote Work from Vietnam: The Key to Balancing Family Accompaniment and Career Continuity