Accounting treatment and internal management responses concerning Circular 99/2025/TT-BTC, applicable from January 1, 2026

2026/06/19

- I-GLOCAL.CO.,LTD Ho Chi Minh City Office

- Hoang Thi Yen Chi

Executive Summary

① Overview — Circular 99/2025/TT-BTC applies from fiscal years beginning on or after January 1, 2026; it permits flexible accounting practice but requires companies to be able to reasonably explain their accounting and management systems.

② Accounting policy regulations — Required where a company deviates from Circular 99’s standard forms (vouchers, chart of accounts, books, financial statements).

③ Internal management regulations — Not mandatory, but Circular 99 presupposes internal rules (e.g., signing authority under Article 10, advance payments under Account 141), so preparation is recommended.

④ Risks if not prepared — Weak explanatory grounds or unclear approval authority can lead to denial of VAT deduction, tax incentives, and CIT deductibility, and affect the audit opinion.

⑤ Format & timing — No prescribed form; prepare to suit the company, ideally before the FY2026 financial statement audit.

Introduction

Circular 99/2025/TT-BTC (“Circular 99”) applies from the fiscal year beginning on or after January 1, 2026, and constitutes a framework that broadly permits flexible operation in accounting practice. Companies are required to maintain a state in which they can reasonably explain their own accounting treatment and management systems. In light of Circular 99, this article organizes the points of practical response that a company should have in place with respect to its accounting policy regulations and internal management regulations.

1. Approach to the preparation of regulations under Circular 99

1-1 Accounting policy regulations

Under Circular 99, standard forms are prescribed for accounting vouchers, the chart of accounts, accounting books, and financial statements. Where a company independently designs, or modifies or adds to, these, it is required to prepare accounting policy regulations (or equivalent documentation) that clarify the company’s policy as to the necessity and content of such measures.

Specifically, this applies in cases such as the following:

• Where the form of an accounting voucher is newly created, or modified or added

• Where the name, number, structure, or content of an account is modified or added

• Where the form of an accounting book is newly created, or modified or added

• Where a presentation item is added to the financial statements

In practice, companies operating in complete conformity with Circular 99 are not numerous, and it is common for some independent treatment to be adopted in part. An example is a case where accounts are subdivided in order to manage time deposits by currency. Where a company carries out operation that differs from the standard forms of Circular 99 in this way, it is desirable to prepare accounting policy regulations in order to ensure the consistency of accounting treatment and to be in a state where the company can also explain itself to the authorities and others.

1-2 Internal management regulations

Under Circular 99, a company is to bear responsibility for clarifying the authority, roles, and responsibilities of the relevant departments and individuals with respect to the internal flow in transactions, and for operating appropriate internal controls. For this reason, a company is required to prepare and operate, as internal management regulations (or equivalent documentation), a management and checking mechanism that suits its own practice.

With respect to internal management regulations, a clear obligation to prepare them—such as “they must necessarily be created when a particular form is changed”—is not stipulated, as it is for accounting policy regulations. However, Circular 99 establishes several provisions that presuppose the existence of internal management regulations, and in practice it is assumed that certain internal rules are documented, such as in regulations.

Specifically, with respect to such matters as the treatment of signing authority for accounting vouchers (Article 10) and the procedures for advance-payment processing by employees (Appendix II, Account 141), it is presupposed that the internal approval flow and division of responsibility are clear. It should be noted that, where internal rules are not organized with respect to these matters, the company may be requested by the tax authorities or auditors to explain the legitimacy of transactions and its management system.

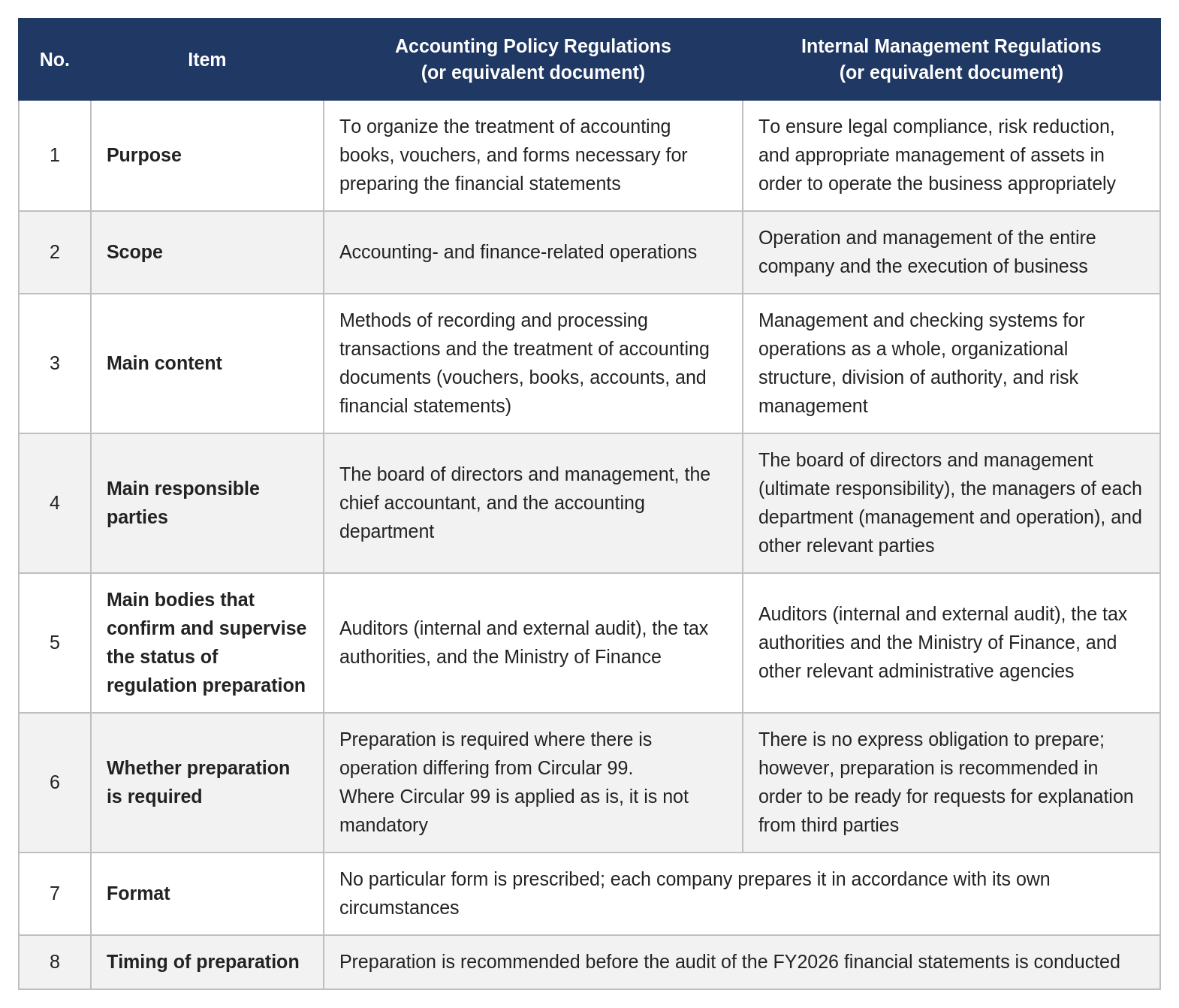

2. Comparison of accounting policy regulations and internal management regulations

In light of Circular 99, the main points concerning accounting policy regulations and internal management regulations are compared and organized below.

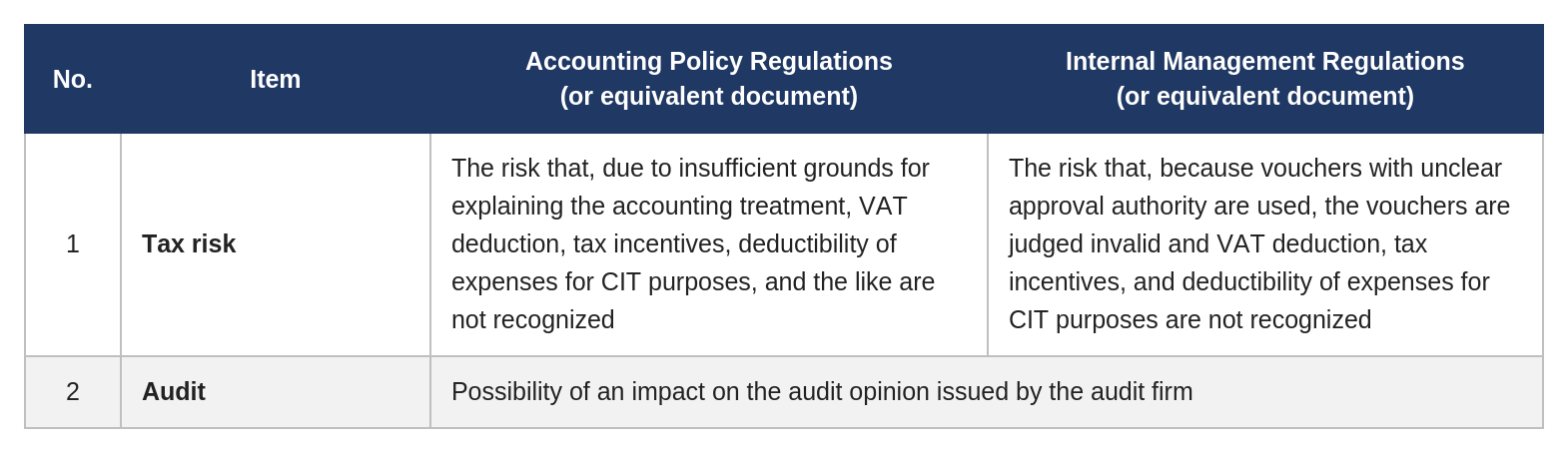

3.Anticipated impact where regulations are not prepared

Conclusion

The preparation of accounting policy regulations and internal management regulations in light of Circular 99 has significance not in remaining a merely formal response, but in the point that it organizes the accounting treatment and management system that the company has adopted and secures a state in which the company can explain itself to third parties. At the present time, uniform preparation of regulations is not required of all companies; however, in practice there are not a few situations in which treatment presupposing the existence of regulations is assumed. It is important for a company, while keeping a close watch on future trends in the operation of the system, to carry out the preparation and review of regulations in accordance with its own practice.

References

・Circular 99/2025/TT-BTC

Related Reports

・Explanation of Key Points in Tax and Accounting Reforms in Vietnam in 2025