The Latest Practices on Methods of Returning Funds to the Parent Company and "Capital Reduction" in Vietnamese Subsidiaries

2025/04/30

- I-GLOCAL CO., LTD Hanoi Office

- Certified Fraud Examiner

- Kiriko Kashima

Introduction

Although “capital reduction” is legally permitted in Vietnam, practical cases are rare, and the procedure has long been recognized as complicated and highly difficult.Therefore, many companies have operated on the assumption that executing capital reduction is difficult, typically setting low capital amounts at the time of company establishment and carefully selecting funding and return methods.However, in recent years, there have been an increasing number of cases where companies carry out capital reductions, and the related practical procedures are gradually being established.This article focuses on capital reduction as a means of returning funds from Vietnam to parent companies and explains the latest system trends and practical points to consider.

1.Means of repatriating funds from the Vietnamese subsidiary to the parent company

There are various methods for repatriating funds from a Vietnamese subsidiary to the parent company, but currently, the following three are mainly used in practice.

First, let’s organize the characteristics of each method in the table below.

<Comparison of Major Capital Return Methods>

| Methods of Fund Repayment | Content | Practical Considerations |

| Dividend remittance | Transfer the retained earnings, which remain after the corporate tax declaration and payment, to the parent company.This is typically done once every six months to one year. | ・The amount of dividends is limited to “retained earnings” after fulfilling tax obligations. ・In Vietnam, no dividend tax is imposed; in Japan, 95% of the dividends can be treated as tax-exempt under certain conditions. ・Remittances in foreign currency are also permitted. |

| Service / Royalty Agreement | ◆Service Agreement: Payment for management, guidance, and support costs. ◆Royalty Agreement: Payment for brand and technology usage fees. |

・It is necessary to properly prepare supporting documents such as contracts, invoices, and payment certificates. ・Service fees are subject to foreign contractor tax (5% CIT + 5% VAT), and royalties are subject to 10% CIT. ・If the service fees are excessively high, there may be risks related to transfer pricing regulations. ・Supporting documents proving the nature of the headquarters’ assistance are required. |

| Parent-child loan interest | A loan agreement (parent-child loan) is made from the headquarters to the Vietnam subsidiary, and foreign currency remittances are made in the form of principal plus interest repayments. | ・If the borrowing period exceeds one year, the loan must be registered with the State Bank of Vietnam. ・Interest is subject to foreign contractor tax. ・Because there is a risk under the transfer pricing tax regime, the borrowing interest rate must be aligned with the market level. ・The interest amount itself is not expected to be large, so its impact as a method of return is limited. |

Dividend remittances are the most common means of returning capital.

Although limited to retained earnings, they are widely used due to tax advantages.

On the other hand, interest payments on service/royalty agreements and parent-subsidiary loans are subject to taxation, and attention must also be paid to transfer pricing risks and documentation preparation.

Although capital reduction has not been widely utilized until now, it has attracted attention in recent years as a feasible method if certain requirements are met.

The next chapter explains its legal framework and practical procedures.

2.“Capital Reduction” Related Laws and Objectives

2-1. Legal reforms in corporate law

The 2020 Vietnam Enterprise Law stipulates the following conditions under which a limited liability company can reduce its capital.

Since a capital reduction aimed at returning funds falls under Case 1 described below, this article explains based on Case 1.

<Types of Capital Reduction and Points to Note>

| Types of Capital Reduction | Conditions | Points to Note |

| Case1: In case of refunding part of the share to the investor |

・The business has been continuously operating for more than two years since its establishment. ・Even after the refund, it can fully fulfill all debts and financial obligations. ・Target: Single-member limited company and limited company with two or more members. |

・Capital reduction of the articles of incorporation is not allowed during the first two years from the start of business. ・In the case of a limited company with two or more shareholders, each shareholder must simultaneously reduce capital in the same proportion. |

| Case2: When a company buys back part of a shareholder’s equity interest |

・Investors who oppose important resolutions such as changes to specific items in the articles of incorporation or organizational restructuring can request the repurchase of their shares within 15 days from the date of the resolution. ・Even after the repurchase, they can fully meet all debts and financial obligations. ・Applicable to: limited liability companies with two or more members. |

If the financial conditions are not met, the investor who has requested the buyback of their equity interest may transfer that interest to other investors or third parties. In this case, no capital reduction will occur. |

| Case3: If the capital stated in the articles of incorporation is not fully paid in by the deadline |

・If the full amount of the capital is not paid within 90 days after the issuance of the Enterprise Registration Certificate (ERC), a procedure to reduce the unpaid portion is required. ・Applicable: Single-member limited company and limited companies with two or more members |

Delays in capital payments and fluctuations in exchange rates often occur in the early stages of establishment. |

※Capital reduction by joint-stock companies also became possible under the 2020 Corporate Law, but this article will omit the explanation.

A major advantage is that remittances through capital reduction are classified as capital return and therefore are not subject to taxation in Vietnam.

On the other hand, the cases where capital reduction cannot be done or is restricted are as follows.

・When there are accumulated losses

・In industries with minimum capital requirements (such as real estate, finance, etc.)

・When receiving investment incentives (because the incentive conditions would no longer be met)

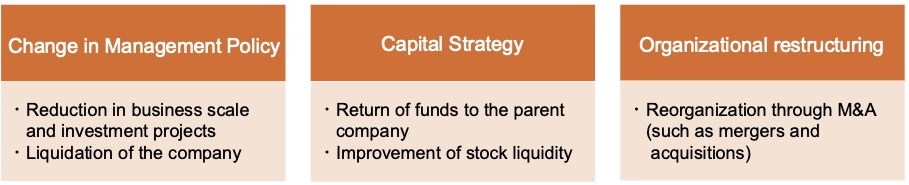

2-2. Purpose of a company reducing its capital

First of all, there are generally three main reasons why a Vietnamese corporation would consider reducing its capital.

In Japan, capital reduction is often perceived as an action based on negative reasons such as declining sales or deteriorating earnings, raising concerns about risks like falling stock prices and impacts on shareholders due to the impression of poor management.

On the other hand, in Vietnam, under the law, if retained earnings are insufficient, it is not possible to apply for capital reduction in the first place.

Therefore, in practice, capital reduction can be considered as a proactive measure aimed at capital strategy or organizational restructuring.

3. Latest Practical Procedures for Capital Reduction Application and Bank Transfer

Regarding Case 1 in Section 2-1 of this paper, there are no statutory provisions for the amount of capital reduction.

Based on our practical experience, the condition for capital reduction that “all debts and financial obligations can be fully performed” can be represented by the following formula, and we interpret this as the maximum allowable amount of capital reduction.

When implementing a capital reduction, it is necessary to apply for the revision of ① the Enterprise Registration Certificate (ERC) and ② the Investment Registration Certificate (IRC) to the competent authority, the Department of Finance (DOF, formerly the Planning and Investment Department). According to the 2020 Enterprise Law, the revision application for the ERC must be submitted within 10 days from the date of the capital reduction; however, in practice, banks often require a revised ERC at the time of remittance for the capital reduction.

In practice, the capital reduction procedures that our company supported in Hanoi and Ho Chi Minh City were carried out according to the following process.

Based on practical cases of capital reduction that our company has supported in the past, the following summarizes the points to note regarding the procedures for amending ERC/IRC and for bank transfers.

<Points to Note Regarding ERC and IRC Amendments to the Department of Finance (DOF)>

・During IRC revisions, there is a strong tendency to be required to explain the rationale for the capital reduction and the future financial outlook.

・In local government offices, there are cases where precedents for capital reduction are scarce. In such cases, the Department of Finance (DOF) may inquire with central cities, such as Hanoi and Ho Chi Minh City, for reference.

Therefore, it is advisable to allow ample time in the schedule, anticipating the possibility that the review period may be extended.

<Points to Consider Regarding Bank Transfer Procedures>

・It is advisable to notify the bank in advance if you plan to send funds due to a capital reduction.

・The documents and procedures required for remittance are determined based on the internal regulations of each bank.

Some banks may require both the amended ERC and IRC when remitting capital reduction funds, so it is essential to confirm in advance with the correspondent bank.

In conclusion

With the emergence of practical cases of “capital reduction,” which was previously recognized as highly difficult, the options for capital planning of Vietnamese subsidiaries have expanded in recent years.

On the other hand, the number of cases is still small, and careful handling is required, so prior negotiations with the competent authorities and the banks involved are essential.

Our company will strengthen support for the capital reduction procedures going forward.

We hope you will refer to this report and feel free to contact us if you have any specific inquiries.

References

2020 Vietnam Enterprise Law

Contact Information

I-GLOCAL CO., LTD. https://www.i-glocal.com/

Person in charge:Kiriko Kashima

kiriko.kashima@i-glocal.com

Ho Chi Minh Office +84-28-3827-8096 Hanoi office +84-24-2220-0334

This article was translated using Yarakuzen.