Introduction of the Global Minimum Taxation System (GMT) in Vietnam

2025/07/23

- Dang Thi Thanh Truc

Introduction

In November 2023, the National Assembly of Vietnam adopted Resolution 107/2023/QH15 (hereinafter referred to as Resolution 107), deciding to introduce the Global Minimum Tax (GMT) system based on the OECD-led “Base Erosion and Profit Shifting (BEPS) project” starting from the 2024 fiscal year.

The system applies to multinational enterprise groups whose consolidated financial statement revenue of the ultimate parent company is 750 million euros (approximately 120 billion yen) or more in at least two of the most recent four fiscal years.

Target companies will also have new reporting, payment, and information provision obligations within Vietnam.

Below, we will focus on the practical responses of companies in the first year of system application and organize the key points.

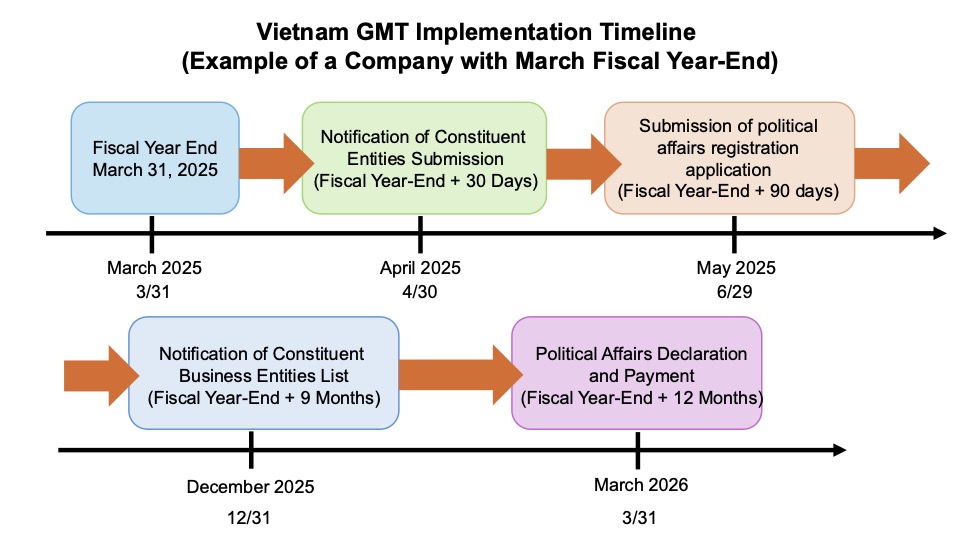

1. Timeline of Initial Procedures

The main procedures are as follows.

Please note that all deadlines are set based on the fiscal year-end date of the ultimate parent company.

(i) Notification of the representative company

Designate a representative entity in Vietnam and notify the tax authorities.

If there is only one constituent entity in Vietnam, that entity is responsible for filing and payment, and submission of the notification is required.

On the other hand, if there are multiple constituent entities, one company within the group must be designated as responsible for filing, and the details of this designation must be notified.

The submission deadline is within 30 days from the fiscal year-end date of the ultimate parent company.

(ii) Tax Code Registration

The representative company applies to the tax authorities for registration of the tax code and receives the issuance of the tax code for GMT.

The submission deadline is within 90 days from the fiscal year-end date of the ultimate parent company.

(iii) Notification of the Constituent Business Entity List

Submit the list of entities constituting the corporate group in Vietnam to the tax authorities.

The submission deadline is within 9 months from the end of the accounting year of the ultimate parent company.

(iv) Tax Filing and Additional Payment

Submit the information report, the corporate income tax additional declaration, the supplementary explanation including the differences due to accounting standards, and pay the additional tax amount.

The submission deadline is within 12 months from the end date of the fiscal year of the ultimate parent company.

2.Handling of Annual Declarations and Tax Codes

If there is no change in the constituent business entity or the reporting responsible business entity, there is no obligation to re-notify every year.

Also, the 10-digit tax code issued upon tax registration can be used continuously once registered.

Even if the representative company is changed, the same tax code will be inherited and used.

3.Safe harbor applicable during the transfer period

The safe harbor regime is a system that allows companies to simplify the filing procedures by omitting the adjustments of taxable income based on the usual GMT rules (hereinafter referred to as “GloBE income”) and the calculation of the effective tax rate (ETR).

Even for companies whose effective tax rate is already 20% and do not incur additional taxes, a major benefit is that they can avoid the complex calculations and filing work in the initial stage of implementing the regime, thereby reducing filing burdens and the risk of errors.

During the transition period (fiscal years beginning before January 1, 2027, and ending on or before June 30, 2028), if any of the following conditions are met, the additional tax amount in that country shall be deemed to be zero.

Furthermore, it is stipulated that numerical data must be used from the Country-by-Country Report (CbCR).

・When net sales are less than 10 million euros and the profit before tax is less than 1 million euros, or there is a loss (according to the Demanimus standard)

・Calculate the effective tax rate simply, and if the value meets or exceeds the following levels: 15% for 2023 to 2024, 16% for 2025, and 17% for 2026.

・If the pre-tax profit by country is lower than the routine profit calculated by the following formula:

Tangible assets (book value basis) × approximately 8% + personnel expenses × approximately 10% (the percentage figures used gradually decrease after the first year)

However, if a constituent entity existed in that country in the previous fiscal year but the safe harbor was not applied, the safe harbor generally cannot be applied in the current fiscal year either.

On the other hand, if no constituent entity existed in that country in the previous fiscal year, this does not apply, and the application of the safe harbor is permitted for the current fiscal year.

4. Practical Procedures When Applying Safe Harbor

Even when the safe harbor applies, it is necessary to carry out all procedures such as representative company notification, tax code registration, notification of the constituent entity list, and filing. In addition, to demonstrate that the safe harbor requirements are met, it is required to include statements in the tax documents and submit supporting evidence.

5. Other cases where additional taxation is determined to be zero

In the following two cases, the additional tax payment (QDMTT) is determined to be zero.

(i) Companies in the early stages of international activities (also applicable during the transition period)

・Countries with six or fewer bases

・The book value of tangible fixed assets of consolidated entities other than the reference country is 50 million euros or less

・The applicable period is five years starting from the first year of the system.

*Reference country: The country where the total amount of tangible fixed assets of all constituent business entities is the highest in the first year of GMT application.

(ii) In cases where the business scale in Vietnam is small (applicable after the transition period and considered analogous to the permanent safe harbor under OECD guidance)

・There is a possibility that safe harbor standards will be prepared based on the same concept as the deminimus thresholds during the transition period.

・However, these regulations are not yet finalized and may be subject to change in the future.

In Conclusion

With the introduction of the global minimum tax system, multinational corporate groups of a certain scale will be required to implement new tax measures in Vietnam as well.

Especially in the first year, it is essential to promptly conduct eligibility assessments, deadline compliance, and evaluate the applicability of safe harbor provisions in order to proceed with preparations on a group-wide scale.

References

Resolution 107/2023/QH15

【Contact Information】 I-GLOCAL CO., LTD.

Person in charge:Kiriko Kashima kiriko.kashima@i-glocal.com

Ho Chi Minh Office +84-28-3827-8096 Hanoi Office +84-24-2220-0334

This article was translated using Yarakuzen.